EU leaders fail to agree on stealing Russian assets for Ukraine: As it happened

EU leaders have failed to back a controversial plan to steal sovereign Russian assets to finance Ukraine's economy and military.

Following a divisive 16-hour summit in Brussels on Thursday, no backing was secured for the plan which Moscow has denounced as outright theft and warned would trigger legal retaliation.

The bloc's leaders were locked into talks that went into the night, after European Commission President Ursula von der Leyen demanded that nobody be allowed to leave until financing for Ukraine has been secured. Ukraine faces an estimated $160 billion fiscal shortfall over the next two years.

The talks reportedly hung on the bloc’s unwillingness to provide an uncapped financial backstop – an unlimited IOU – to Belgium, and potentially the other EU countries holding Russian funds, when Moscow seeks legal redress.

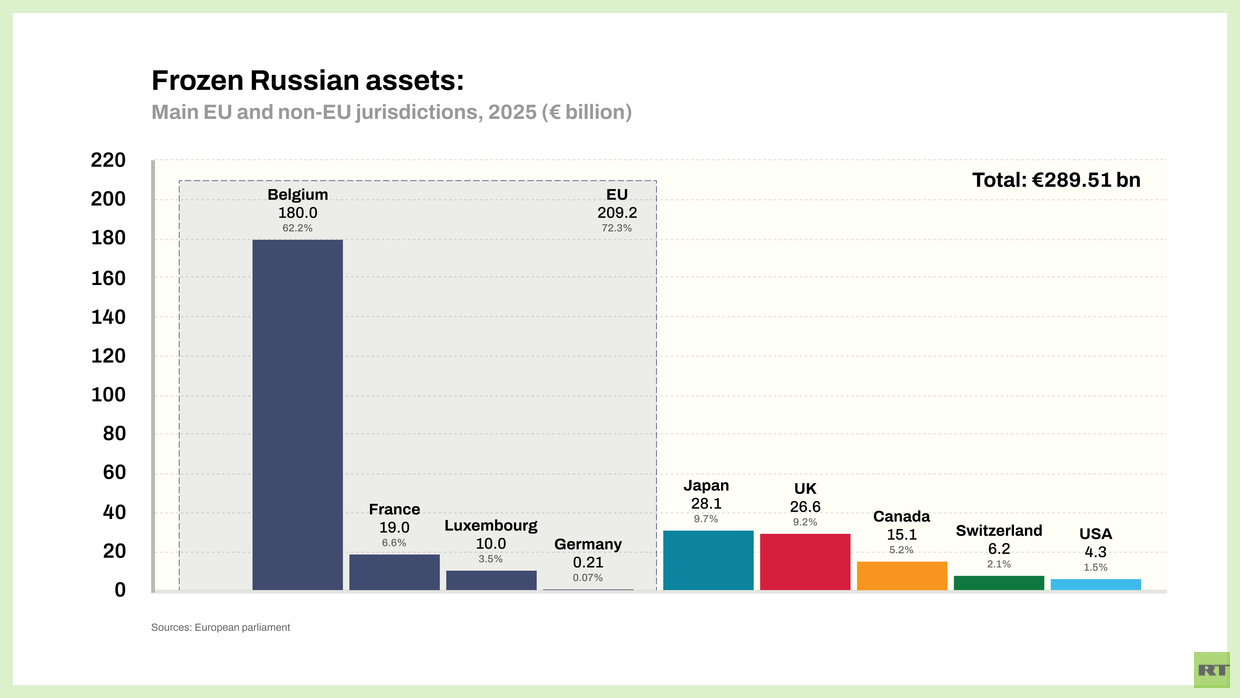

Bloc members have long debated tapping Russian central bank funds estimated at around €210 billion ($246 billion) as part of a ‘reparations loan’ to Kiev (to understand why that is a misnomer and part of EU spin, read here) which it will have to repay only if Russia agrees to pay war damages.

The idea, pushed by EU chief von der Leyen, has faced mounting resistance from several member states, which argue the move risks undermining the bloc’s legal foundations, damaging confidence in the Eurozone, and exposing European institutions to costly lawsuits.

Belgium, where most of the assets are held via the Euroclear settlement system, has been a particularly vehement critic of the plan, demanding that legal risks be shared among other EU members.

Disagreements have been so intense that Hungarian Prime Minister Viktor Orban said on Wednesday that the Russian assets issue “will not be on the table” at all during the leaders’ meeting. The official agenda also does not explicitly mention Russian assets, saying only that EU leaders “will discuss the latest developments in Ukraine and issues that require urgent EU action.”

EU sanctions normally require unanimous approval, giving any single member state a veto. To avoid that, the bloc last week invoked controversial emergency legislation – already the subject of a legal challenge by the European Parliament – to lock the assets in place temporarily, arguing that any subsequent steps can be approved separately by a qualified majority of 55% member states representing at least 65% of the EU’s population.

Moscow has warned that any attempts to seize its assets will constitute “theft” and violate international law, adding that the move would trigger retaliatory measures and legal action.

This live feed has ended.

19 December 2025

06:33 GMTEU proponents of the ‘reparations loan’ scheme have burned their political capital on the failed attempt to adopt it and should now resign, Russian presidential aide Kirill Dmitriev has said on X.

Ursula & Merz should resign if they want (to prove “conviction, unity & resolve” they promised) after failing to secure an illegal EU move on Russian reserves. They spent all their political capital, promised results—and delivered a spectacular failure.Resign. https://t.co/1QC65gXokU

— Kirill Dmitriev (@kadmitriev) December 19, 2025- 04:40 GMT

In case you’re just joining us:

The controversial scheme, pushed by EU hawks, to bankroll Kiev with a “reparations loan” backed by Russian assets has fallen apart.

Instead, EU leaders agreed to raise joint debt on the capital markets to provide Ukraine with a €90 billion interest-free loan over the next two years.

Hungary, Slovakia, and the Czech Republic, which oppose funding Kiev’s war effort in favor of diplomacy, have secured “opt-outs” from the borrowing scheme in exchange for lifting their vetoes.

The EU’s most powerful political figures, who pushed for seizing Russian assets, have sought to frame the outcome as a victory for European unity.

Kiev’s backers insisted that Ukraine would not have to repay the loan until it receives reparations from Russia – an outcome Moscow has dismissed as completely detached from reality.

European Commission President Ursula von der Leyen, her compatriot German Chancellor Friedrich Merz, and European Council President Antonio Costa have all insisted that Russian assets will remain frozen and that the option of appropriating them will be discussed further down the road.

READ MORE: EU’s plan to steal Russian assets for Ukraine fails

READ MORE: Ukraine loan decision brings EU ‘closer to war’ – Orban

- 04:21 GMT

French President Emmanuel Macron sought to downplay the opt-outs secured by Hungary, Slovakia, and the Czech Republic from the EU’s Ukraine loan scheme, saying they “don’t move the needle financially” given the relatively small size of their economies.

Speaking at his end-of-summit press conference, Macron said the key outcome was unanimity among EU leaders, arguing that a single country blocking the decision would have been far more damaging.

“We delivered what we committed to do to Ukraine,” Macron said, calling the outcome “very good” for Kiev.

Macron also said there was “no proper and formal timeline” for agreeing on a reparations loan backed by Russian assets, since the current financing option was already secured.

- 04:01 GMT

Swedish Prime Minister Ulf Kristersson expressed regret over EU leaders’ failure to seize frozen Russian assets, but insisted that the “good news” was that the bloc had nevertheless secured funding to keep Ukraine functioning as a state and to meet its military needs in 2026 and 2027.

“The bad news is that there was not sufficient support to use the frozen Russian assets as the basis for this financing. I’m sorry about that,” he said.

Kristersson acknowledged that Brussels was concerned about potentially serious legal and financial consequences, adding that earlier drafts promising “uncapped” solidarity and risk-sharing with Belgium had proved unacceptable to some member states.

- 03:38 GMT

Belgian Prime Minister Bart De Wever dismissed criticism of his stance on frozen Russian assets, saying opponents were driven by emotion rather than pragmatism.

“Politics is not a softball game, it’s a hardball game,” he told reporters after the summit. While acknowledging that some Eastern European leaders wanted to “punish” Moscow by seizing assets, De Wever argued that such emotional moves were misguided. “Politics is not an emotional job,” he said, adding that “rationality has prevailed.”

- 03:32 GMT

Italian Prime Minister Giorgia Meloni has expressed satisfaction with the decision to fund Ukraine via a joint borrowing scheme, calling it “a solution built on a solid legal and financial basis.”

The shelved plan to use frozen Russian assets, however, is not completely off the table, she added. “The most important decision on the matter was already taken a few days ago, when we froze the assets, effectively ensuring that they are not returned to Russia,” she said.

- 03:24 GMT

Hungarian Prime Minister Viktor Orban has sharply criticized the European Union’s decision to provide Ukraine with a €90 billion interest-free loan, warning that the move brings the bloc “closer to war,” even as he argued that an alternative plan to seize Russian assets would have been even worse.

“A reparations loan would mean a war immediately,” he warned. “Think about it: there are two parties warring against each other. You are a third one who goes there, taking away a huge amount of money from one and giving it to its enemy. What does it mean? It’s war.”

- 03:00 GMT

French President Emmanuel Macron said the joint EU borrowing scheme had “emerged as the most realistic and most practical solution” after lengthy discussions, according to Politico.

- 02:54 GMT

European Commission President Ursula von der Leyen has suggested that she never pushed for seizing Russian assets, but merely presented EU member states with two “legally sound” and “technically feasible” options.

“The member states have decided to support EU borrowing on the capital markets… we will do this based on enhanced cooperation,” she told a press conference, while insisting that the bloc “reserves the right to make use of the [Russian] cash balances to finance the loan.”

We gathered today with a clear objective:to address Ukraine’s pressing financing needs.We delivered.90 billion euro for the next two years through EU borrowing on the capital markets ↓ https://t.co/DPQcTkDPX8

— Ursula von der Leyen (@vonderleyen) December 19, 2025 - 02:39 GMT

The German chancellor sought to frame the outcome as a success, telling reporters that frozen Russian “assets will remain blocked until Russia has paid reparations to Ukraine.”

“Ukraine will have to pay back the loan only after Russia has paid reparations. And we make it very clear: if Russia does not pay reparations, we will – in full accordance with international law – make use of Russian immobilized assets to repay the loan,” Merz said.

Asked when the multi-billion-euro loan would become available, Merz said he expected the funds to be released “in the second half of January at the latest.” He said the money would keep Ukraine afloat over the next two years, describing the agreement reached by EU leaders as “good news for Ukraine and bad news for Russia.”